That’s what Cryptonary is here for – to educate. In this journal, we will dive deep into inflation, monetary policy, and the relationship between consumer prices and monetary policy.

Now, more than ever (literally), it’s important to understand the background of how we ended up here, and what it all means for both the average person and investors. Sit tight, this is a long one!

Disclaimer: This is not investment nor investment advice. Only you are responsible for any capital-related decisions you make and only you are accountable for the results.

Inflation

Before we talk about the factors that are contributing to inflation, it’s important to understand exactly what inflation is. Simply, inflation is the decline of purchasing power of a currency over a period of time. Essentially, higher prices without matching wage growth. Example:- Sam makes $20,000 a year in 2020.

- The cost of running his appliances, heating his home, mortgage, food, etc. comes to $12,000 per year.

- In 2022 Sam still makes $20,000 per year.

- However, his costs have increased 50% over these 2 years due to inflated prices.

- Now, Sam’s cost of living is $18,000. This leaves him with just $2000 per year to spend on other things like entertainment, non-essential goods, etc.

- Sam’s quality of life has dropped dramatically, and he is now essentially living paycheck-to-paycheck – in only 2 years.

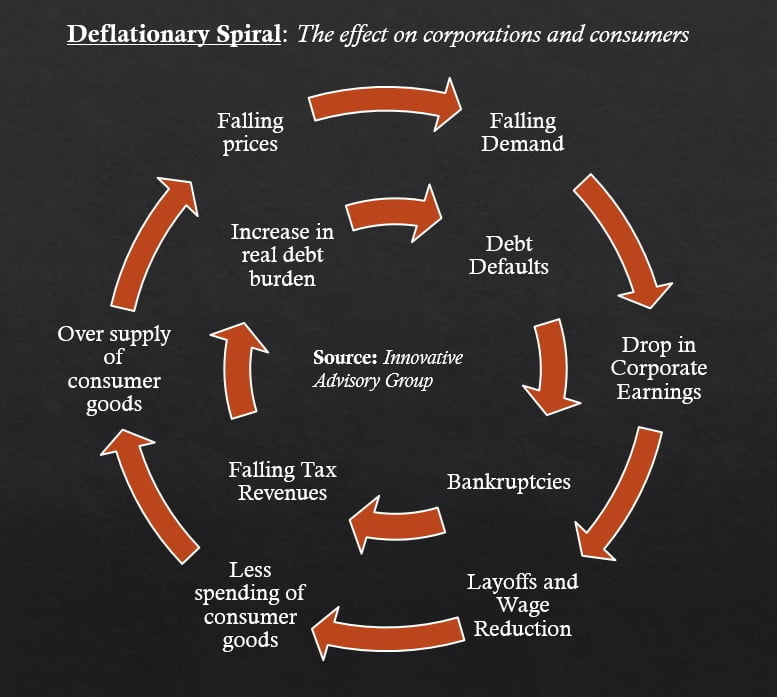

Additionally, inflation is preferable to the alternative – deflation. Deflation has the exact opposite effect described above. If consumers expect prices to fall, they will hold off on spending – why buy something now when it will cost less next year? This is catastrophic for a capitalist economy. Consumers reduce spending, companies lose revenue, factories produce less, people start to lose their jobs, unemployment rises, wages are reduced because the unemployment pool is growing, people can’t afford their mortgages because they don’t have a job – you see where we’re going with this.

Deflation was the main concern that led governments and central banks around the globe to act during the pandemic, reducing interest rates and providing stimulus. So, 2% inflation is the target and is deemed as a fair balance between price increases, manageable wage growth, economic health, and a base reduction in spending power. However, the figures for inflation that we have been seeing for the past couple of years are way beyond 2%. Consumers have seen their purchasing power reduced dramatically, and wages haven’t kept pace – but why?

Inflation Pressures

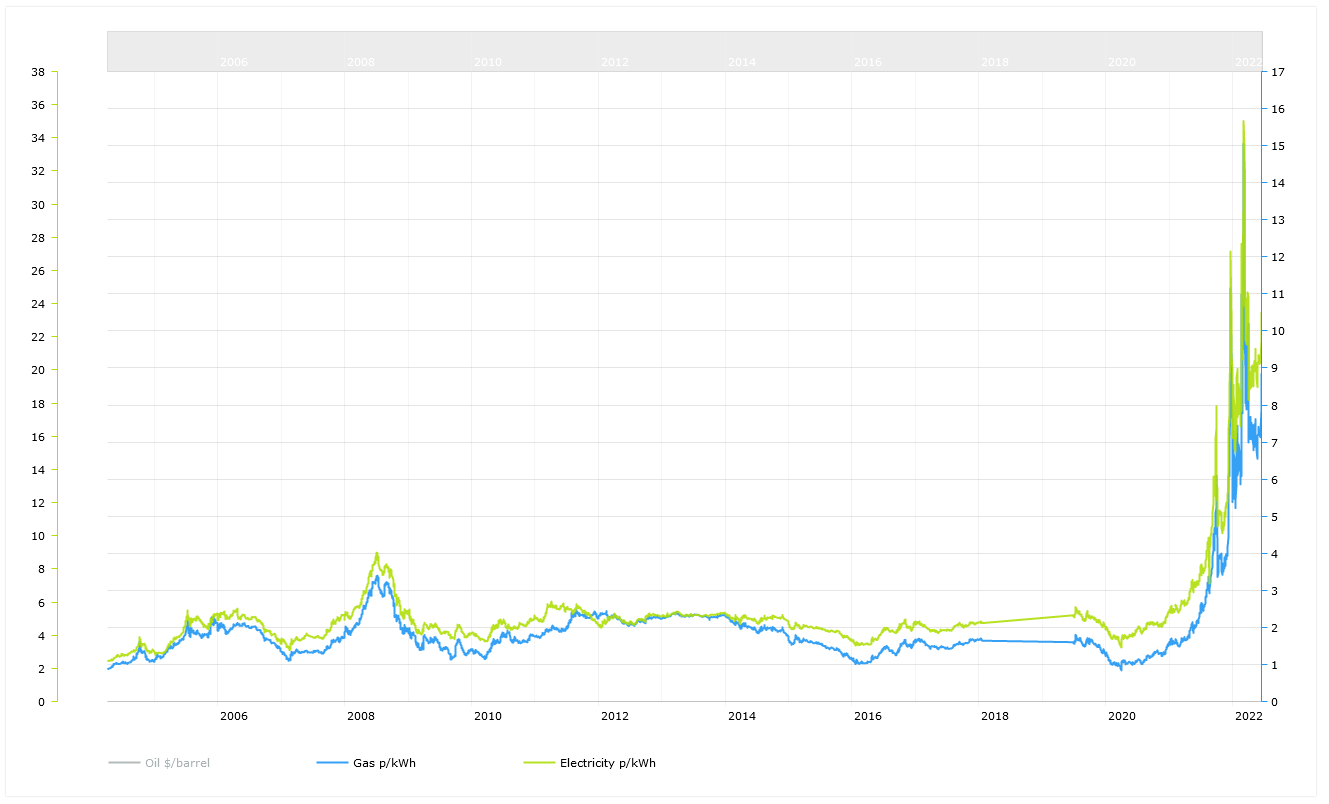

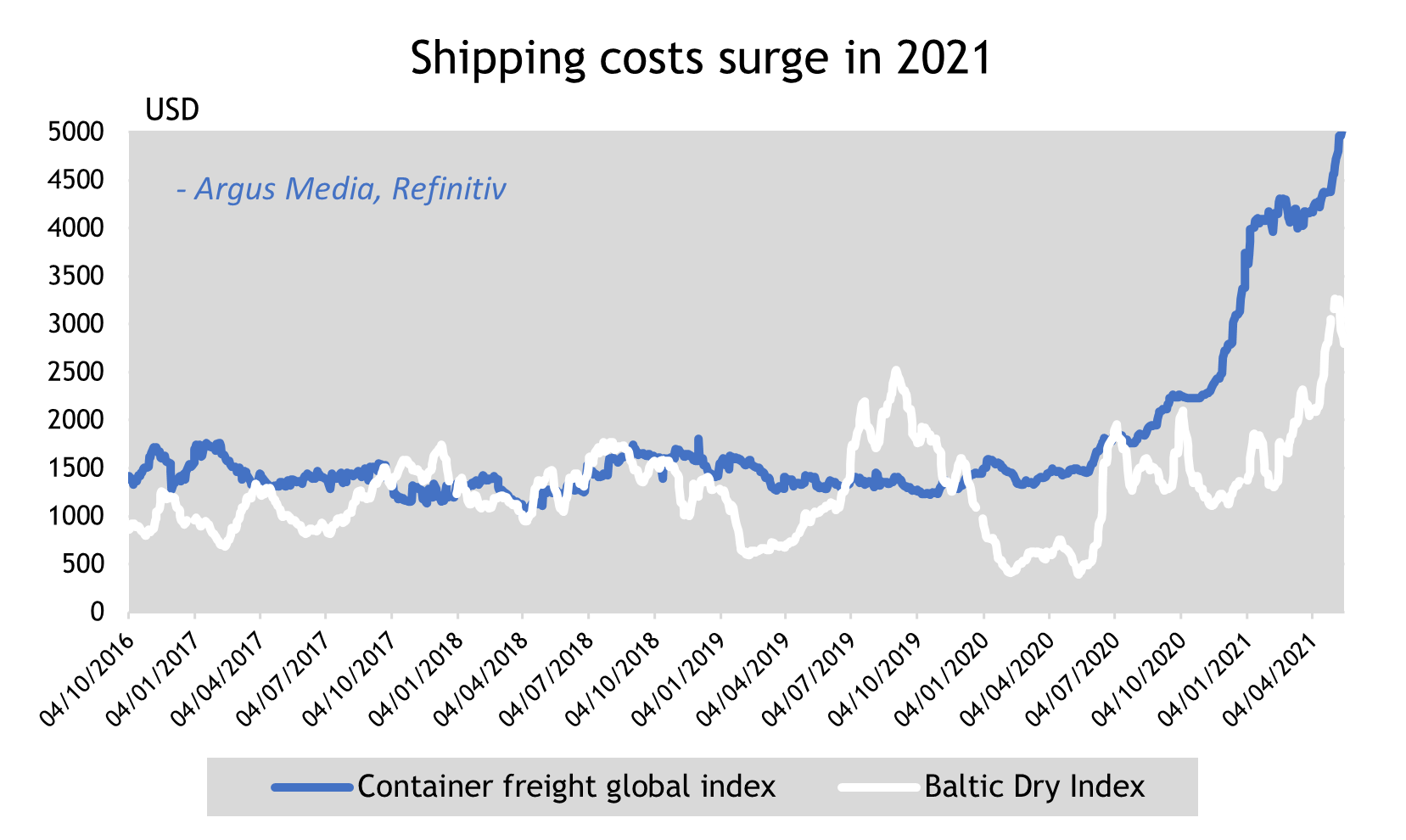

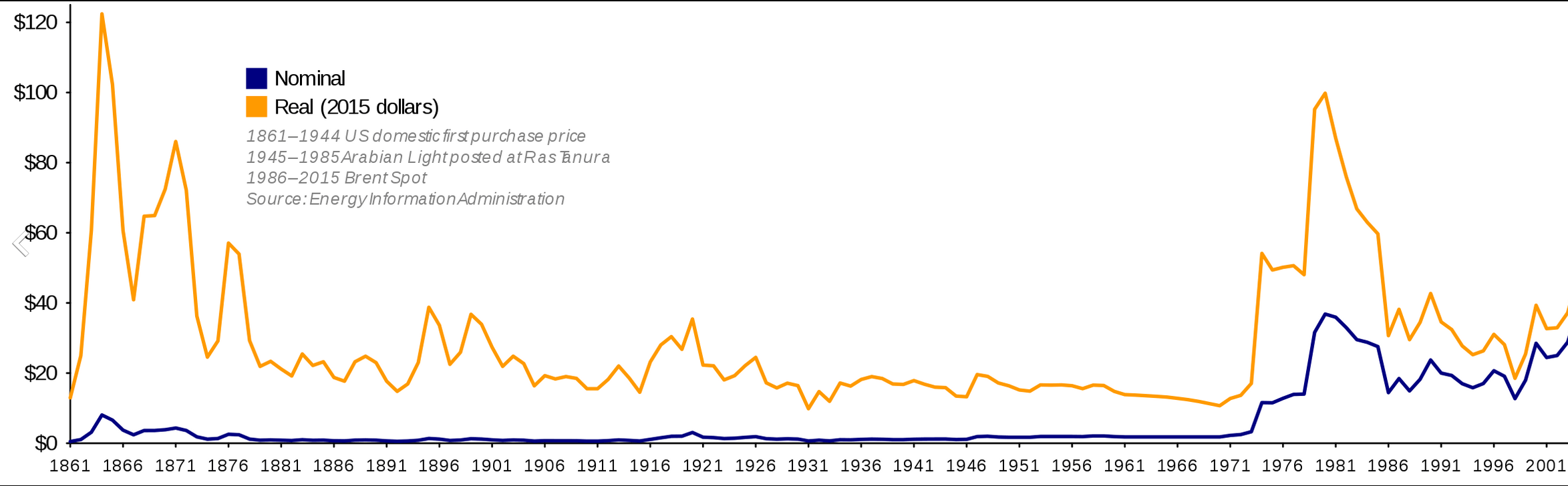

Inflation pressure can come from any number of sources. The most serious cases are usually caused by energy – without cheap energy, everything becomes more expensive. The knock-on effect of more expensive energy (oil, gas, electricity, etc.) affects basically everything we buy as consumers. The most obvious examples are living costs – need to heat a home? Run a washing machine? That’ll cost you 5-10 times as much as it did in 2020.

The above chart shows the extreme extent to which energy costs have increased. What this essentially means is that the purchasing power of wages have been decimated on energy costs alone. Energy costs also inherently increase the price of goods and services.

Nothing can be produced without expending energy in one form or another. Factories use huge amounts of electricity, farming equipment uses huge amounts of petrol/gas – this translates into increased costs for production, transport, etc. and ultimately the bill is passed on to consumers in the form of increased prices. However, the cost of energy is not the only inflation pressure that has eaten away consumer purchasing power.

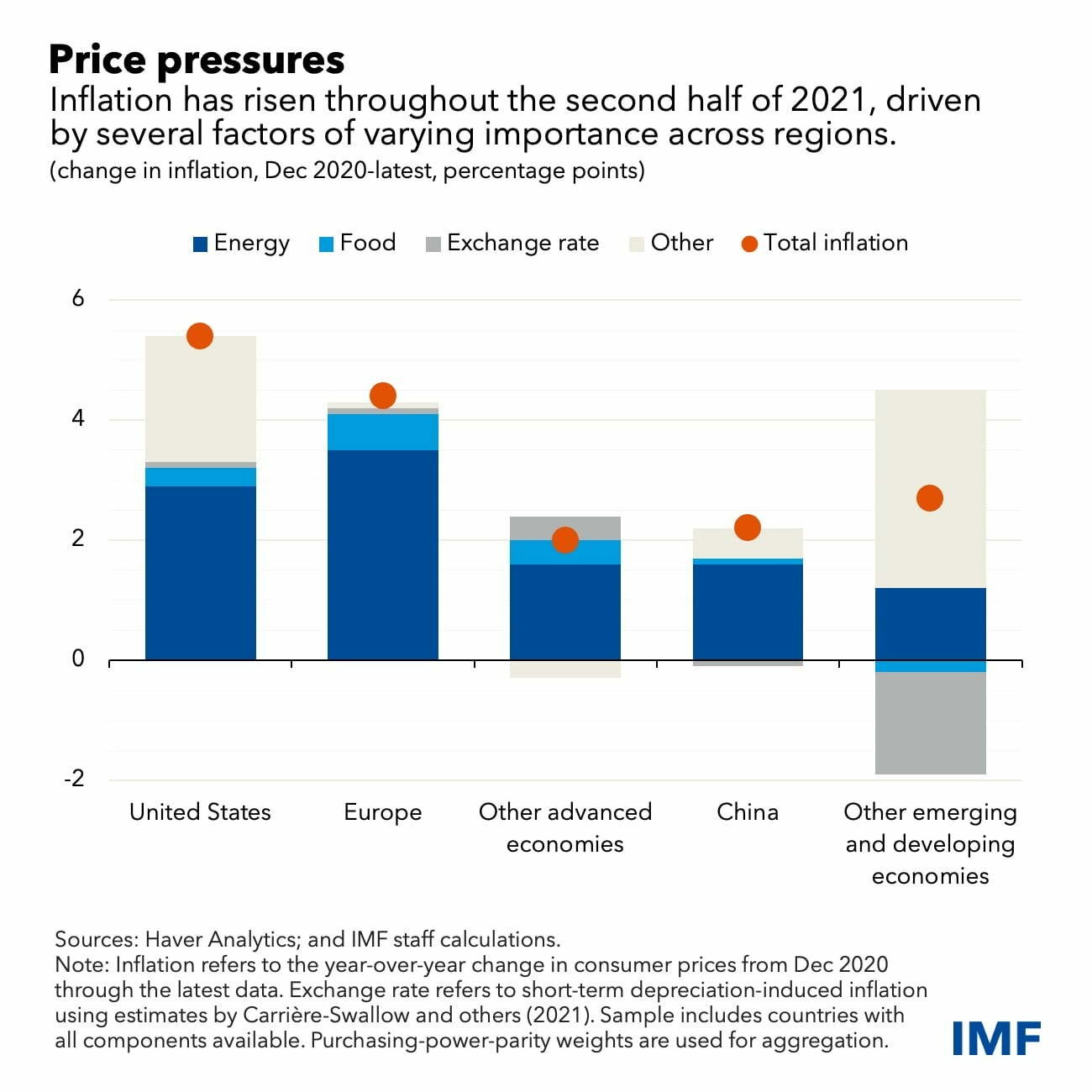

The chart above shows the disparity in where price pressure originates per region. In Europe, for example, energy is by far the largest contributor to inflation. This is largely a result of mainland Europe’s reliance on Russia for natural gas and other energy supplies. Obviously, without a resolution to the ongoing Ukraine-Russia conflict, this is set to continue for the foreseeable future as relations are not great (understatement).

Another key factor is the global food supply. Ukraine has been known for centuries as the “bread-basket of Europe”; some might say even the world – accounting for 9% of global wheat trade. The conflict in Ukraine has dramatically reduced exports due to blockades and the general chaos that conflict brings.

The conflict in Ukraine has increased the cost of food – not because the demand has increased, but because supply has been affected. Additionally, Russia’s share of food exports to Europe has been dramatically reduced because of sanctions from both sides. Overall, this has led to a relatively steep cost in food prices around the world and the situation is not likely to improve until the conflict is resolved and both countries restore exports to pre-War levels.

On a related point, the US and its allies are constructing silos in the Western parts of Ukraine to enable exports through a land corridor to circumvent blockades. However, this infrastructure will likely not be complete till later this year and still does not account for lost production due to destroyed infrastructure.

Supply Chains

In the US, energy is still a large contributor to inflation, but other factors include supply chain issues that increase the cost of shipping goods to the US – higher import prices, basically. The US relies heavily on imported goods to meet consumer demand and the result of high import prices is inflated prices for the end consumer. Supply chains have been under extreme pressure from the effects of COVID and continuing lockdowns in key industrial exporters in Asia, along with high demand for shipping that existing capabilities around the world are struggling to meet.

The issue is not producing enough goods to meet demand – factories are more than able to produce the required goods, at an acceptable cost. However, the issue is that all these produced goods are stuck in ports due to a number of factors:

- Higher demand for goods as the world comes out of lockdown and begins spending again.

- Limited cargo capacity – there is a limit to the number of ships available and the quantity of goods they can carry. This leads to delays at ports, and increased costs per ton since shipping is in high demand.

- Workforce shortage – COVID lockdowns prevent workers from going to work, in addition to companies laying off workers due to reduced demand during the global lockdowns.

Gone are the days of empty shelves in supermarkets during lockdown – those shelves have been replenished, but at what cost? A cost that is increasing every week, and until the supply chain issue is resolved or at least mitigated, it is unlikely we see any slowdown in inflation from this source.

Historical Precedent

This is not the only time in history that there has been a huge disruption to the global economy. Do we have a point in time that the current climate is comparable to? We certainly do! The Nixon Shock.

Before we get into the Nixon Shock, it’s important to understand the historical context. From around 1958 the global financial system was governed by the Bretton Woods system which was agreed upon by 44 countries towards the end of World War II. Here are the key points:

- All countries within the Bretton Woods system agreed to a fixed peg against the US dollar, essentially setting USD as the global reserve currency. This was achieved by each country using their currency to buy/sell USD to maintain the peg.

- This improved international trade relations because it reduced currency volatility, making it easier for companies to set prices and costs for goods.

- The World Bank and the International Monetary Fund (IMF) were set up as a direct consequence, with the purpose of identifying countries that required financial support in the aftermath of the war.

- At this time the US dollar was directly convertible to gold.

In 1966, external (non-US) central banks held $14 billion in USD, whereas the US only had $13.2 billion in gold reserves – only $3.2 billion of these reserves were available for redemption, the rest was reserved for domestic holdings. Many countries around the world began exchanging their USD for gold – but there wasn’t enough. The US attempted to devalue its currency to increase the value of its gold reserves – catastrophic for all other currencies as they were, for all intents and purposes, pegged to the USD. This was unacceptable, and (quite rightly) countries began leaving the Bretton Woods system.

At the same time, there was an ongoing energy crisis launched by Arab members of OPEC embargoing oil exports to the US for their support of Israel during the Yom Kippur War.

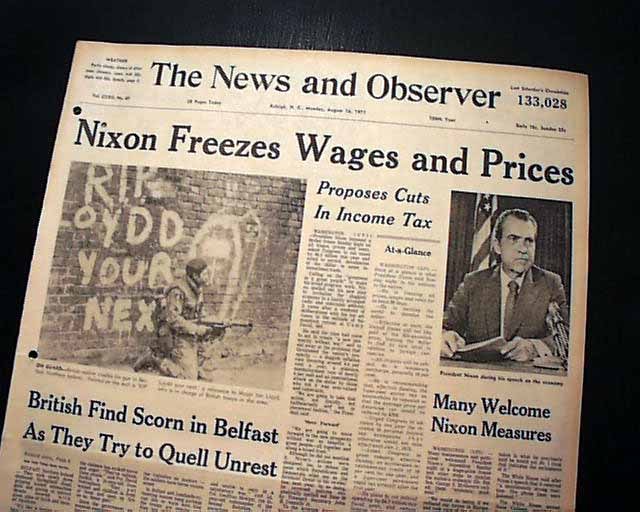

The US at the beginning of the 1970s and throughout had an inflation rate of around 6% and unemployment around 6% as well. Due to the on-going pressure on the USD, the energy crisis, and inflation, President Richard Nixon met with his advisors and came up with a plan:

- The suspension of convertibility of USD to gold.

- A 90-day freeze on wages and prices to counter inflation.

- An import charge of 10% to ensure that products made in the US would not be at a disadvantage due to volatile exchange rates.

From this point on, monetary policy was largely handed to central banks – the creation of new money was no longer dictated by the amount of gold available, but rather by central banks purchasing financial assets of lending money to institutions. In turn, these institutions repurpose this money by offering credit to customers – mortgages, business/personal loans, etc.

When we say that the Federal Reserve is printing money, they are literally creating money out of thin air – we’re not just saying it as an exaggeration.

Now, we’ve covered inflation and how fiat currencies came about - what tools do central banks use to control inflation that is out of hand, in the absence of anything backing the currency?

Interest Rates

Controlling inflation is done by reducing the availability of money. The accessibility of money is largely dictated by interest rates – if money is too expensive to borrow people are less likely to spend. Similar to the point made above about deflation, increasing interest rates reduces the willingness of people and organisations to spend. This reduces demand for goods and services. In turn, businesses reduce the prices of goods and services to try and attract spending. This is called Quantitative Tightening (QT).

Revenues drop, profit margins become tighter, supply outweighs demand, and overall, the economy cools down. The unfortunate consequence of this is that some companies will have to lay people off due to the reduced demand. What central banks try to do when implementing QT is reduce inflation by reducing demand and prices, but at the same time, avoid mass unemployment and a general recession.

The last time the Fed attempted QT was in 2017. From the Great Recession in 2008, interest rates were kept close to 0% - 7 straight years of printing essentially. The QT program of 2017 was cut short in 2019 due to the negative effects on the economy. QT has never been done before on a large scale and its effects are unknown because there is no historical precedent.

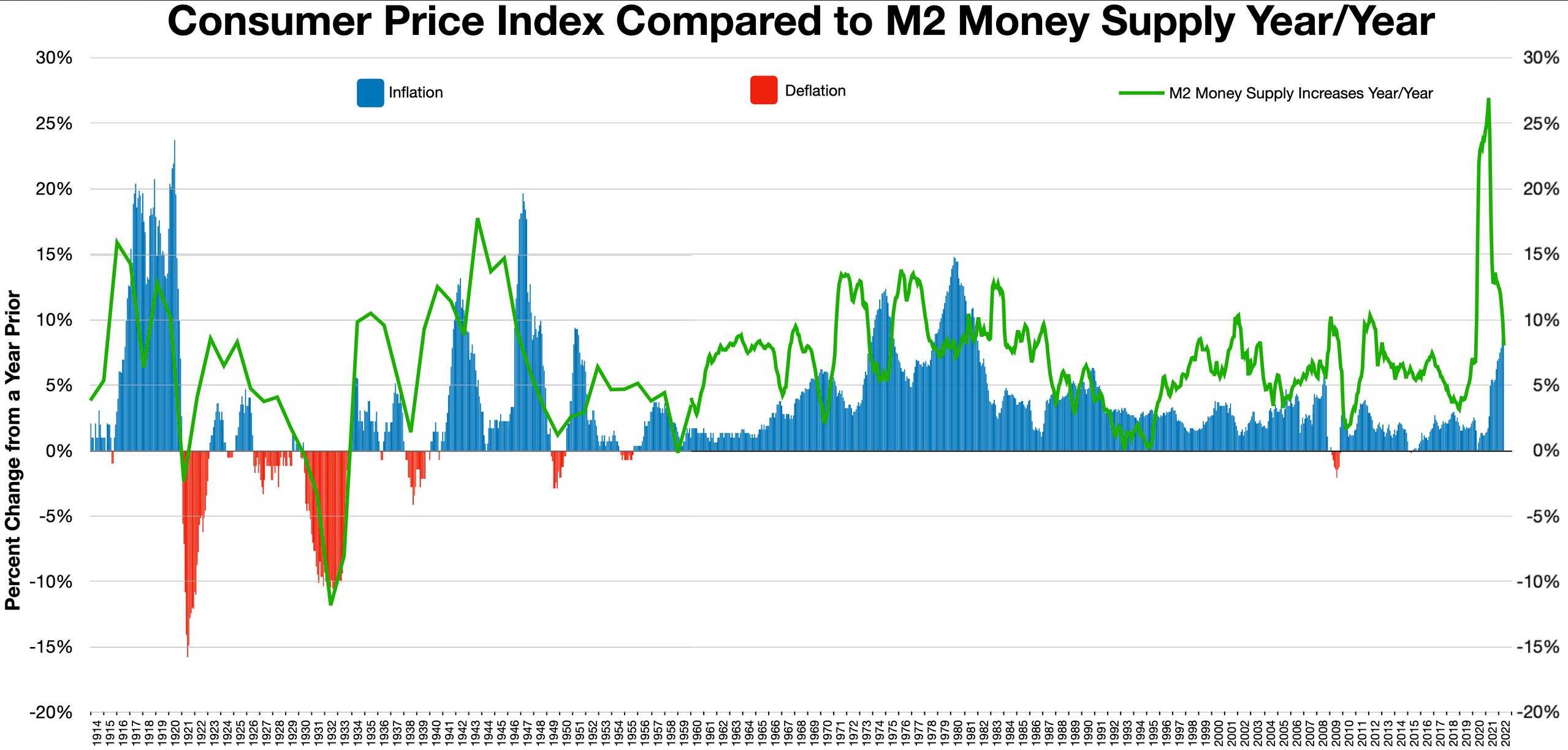

CPI (Consumer Price Index) is a measure of the change in consumer prices over time. M2 money supply is the supply of easily convertible money. As can be seen from the chart above, the dramatic increase in the M2 money supply because of the COVID Quantitative Easing has never been seen before. Subsequently, this policy of QE has been one of the key factors of inflationary pressure over and above the pressures outlined above.

Overall, we believe that the Fed’s hand has been forced into aggressively raising interest rates - largely as a result of its own actions. We believe it is highly unlikely that any sort of risk-on environment will return for at least the next 6-12 months – inflation is simply too high. The Fed has stated on multiple occasions now that tackling inflation is its number one priority – for now it doesn’t look like they are concerned about the outcome in other areas of the economy, such as employment.

Fighting the Fed in this scenario is impossible and so for the remainder of this year into 2023, we will continue evaluating the Feds position and inflation numbers. Ultimately, the US Federal Reserve is in charge of the direction of markets - for now.

Recommended from Cryptonary