Save 23% ($351) & Get a Free 1-1 Call with our Team ⏰ : 0d 2h 59m 44s

How FTX Went Bust & Stole Billions from Users

The unthinkable happened last week – the third largest crypto exchange by volume, FTX, went bust. Sam Bankman-Fried’s operations turned out to be one of the biggest fraud cases and Ponzi schemes ever – even by traditional finance standards. And not only that, Sam’s trading fund – Alameda Research – also went under.

Millions of customers, hundreds of crypto projects, and multiple centralised companies have been locked into Sam’s now-bankrupt empire. Two weeks ago, if you’d asked us which exchange would be insolvent by the end of the week, FTX would have been way down that list.

How could this happen?

The story we are about to tell is one of the most surreal, crazy, unbelievable series of events that has ever hit the crypto markets. It’s not just the effect on the market that’s wild; it’s the chain of events, the lies, the deceit, and the downright degenerate behaviour that led us here too. Strap in and pay attention because the immediate fallout of this collapse is not the only issue crypto will face…

Disclaimer: This is not investment nor investment advice. Only you are responsible for any capital-related decisions you make and only you are accountable for the results.

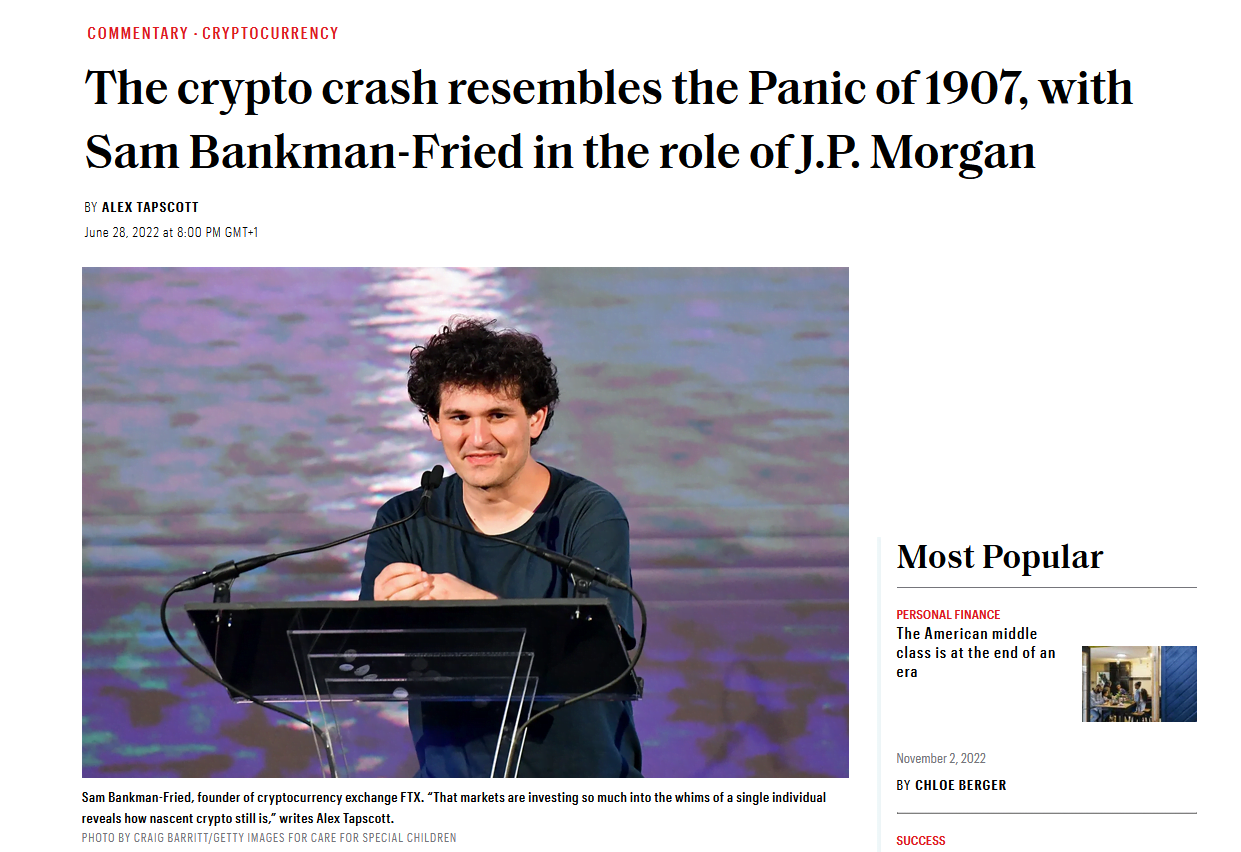

SBF

Before we get into the nitty gritty, it is helpful to have a bit of context when discussing the events of the last week. At the centre of it all is one man – Sam Bankman-Fried. But who is he?SBF began his career in 2013 at a TradFi firm trading ETFs, initially as an intern, but took a full-time position after graduating MIT with a Major in Physics. In 2017, SBF founded Alameda Research, a quantitative trading firm focused on cryptocurrencies. Alameda was the fund through which SBF carried out his famous arbitrage trade, taking advantage of the price difference of BTC between the Japanese and US crypto markets.

In 2019, SBF launched FTX, a cryptocurrency exchange focused on derivatives and leveraged products. Throughout the post-pandemic bull run through 2020 and 2021, FTX became a popular exchange for many investors and traders due to its superior user experience/interface, bespoke derivative products, and relatively tight spread on even the most illiquid altcoins.

Alameda, SBF’s trading firm, was the primary liquidity provider and market maker that operated on FTX (this is where things get spicy, but we’ll get into that a bit later). At Cryptonary, we’ll hold our hands up and say we were huge fans of the exchange and would use it regularly – it did almost everything better compared to competitors like Binance and Kraken.

It was not only the product that was attractive – SBF had a cult of personality behind him. SBF and his peers are (or pretended to be) strong advocates of a philosophical and social movement called effective altruism. Effective altruism is all about prioritising efforts (career, social situations, etc.) into finding the best way to help other people, be it through charity, inventing things, or otherwise.

However, actions speak louder than words, and SBF was indeed acting – in both charitable donations and through his efforts within the crypto market. For instance, in the Summer of 2022 BlockFi and Voyager Digital both ran into issues when Three Arrows Capital (3AC) collapsed due to the fallout from the Terra/LUNA/UST debacle. Thousands of customers were at risk of being locked in these platforms due to bankruptcy. SBF, like a knight in shining armour, came to the rescue and offered loans, bailouts, and direct cash injections of over $735 million to both entities to backstop customer funds and shortfalls in liquidity – what a hero. For the good of the industry, right?

With this kind of disposable income, it would seem unfathomable that FTX was at risk. SBF’s crypto empire appeared to be unstoppable and Sam himself was the poster boy for what it meant to be a good actor within the crypto space. Described by many as the JP Morgan of crypto due to his actions in backstopping the credit crisis that struck crypto earlier this year, Sam built up a reputation of being “the good guy” which is likely why very few individuals saw what was to come next.

Alameda & FTX

There have been rumours for years now surrounding the extent of the relationship between Alameda Research and FTX – SBF was the founder and largest shareholder of both. One rumour was that Alameda Research was using insider information from FTX to front-run trades and listings on FTX Exchange, giving them an unfair advantage. Everyone pretty much knew this was the case, as it would be highly unlikely (given what we know now) for Alameda to be a market maker on FTX without using that sort of information to their advantage.Alameda and FTX were, on paper, supposedly distinct entities. SBF stepped down from Alameda in 2021 to focus on FTX. However, a recent report from crypto compliance firm Argus states that Alameda did indeed use prior knowledge of tokens scheduled for listing on FTX to their advantage, purchasing these tokens and then selling them for profit after the fact. According to the report, from the beginning of 2021 and March 2022, Alameda Research held 18 different tokens for a total of $60 million prior to FTX listing those tokens. These are pretty dirty (illegal) moves from institutions run by individuals who claim to be working towards the betterment of mankind.

Another rumour is that Alameda and FTX conspired to manipulate prices earlier this year to distress competitors and either buy them out or bail them out with strings attached (ie. Voyager, BlockFi, Celsius). Now, none of this is proven as hard fact yet – but considering where markets have ended up and the ongoing situation, as well as what we do know happened, we think it’s likely that all the above is true (and more). This complete lack of morality and predatory behaviour is generally nothing new in the crypto market. However, they are minor infractions compared to the catastrophic revelations that hit markets last week.

FTT Token – SBF’s Achilles Heel

FTT was the exchange token for FTX that allowed holders/stakers certain privileges on the FTX exchange – discounted trading fees, larger allocations on the FTX launchpad, etc. Just your bang average exchange token – if you used the exchange, it’s likely you had a bag of FTT. Now, the exchange token itself was perfectly normal and indeed most other exchanges have their own token as well with varying degrees of utility – CRO (Crypto.com), BNB (Binance), HT (Huobi), etc.

FTT was a token that was created out of thin air and issued by FTX. This is all fine and well - exchanges have the right to create these tokens and offer benefits to those who wish to stake them. However, the FTT token was used for much more than this – and was indeed the key that led to the downfall of both Alameda and FTX.

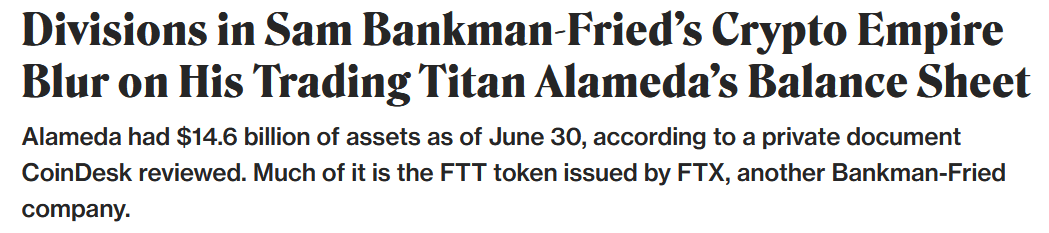

On the 2nd of November 2022, CoinDesk released a report in which they outlined the balance sheet of Alameda Research as of 30th June 2022. On this balance sheet was something odd – something that didn’t make any sense.

Of the $14.6 billion in net assets held by Alameda, $3.66 billion of these assets were held as unlocked FTT. Guess what the third largest holding was? $2.16 billion of FTT collateral.

$5.82 billion of FTT less liabilities (~40% of total assets)? An exchange token that was created out of thin air by Alameda’s sister company? Hmmmmm………

This raised questions – just how separate were Alameda and FTX?

Other notable Alameda holdings on the balance sheet were $292 million of unlocked SOL, $863 million of locked SOL, $41 million of SOL collateral, various other crypto assets (SRM, OXY, FIDA), $134 million cash and equivalents, and $2 billion in equity securities.

Next came the shocker – Alameda had $7.4 billion worth of loans. Alarm bells started ringing. Could it be possible that Alameda had collateralised loans based on, or at least partially based on, the valuation of FTT? There were barely enough other assets (liquid or not) to support that level of borrowing without using FTT collateral – it was highly likely.

We’ve all heard the story from a teacher about the boy who was swinging on his chair, went too far, and cracked his head open.

The idea that one of the most prestigious trading firms in crypto could be swinging on a chair that only had two legs, at the top of Everest, in the middle of a blizzard, started to become too real.

All that was required for disaster was a slight nudge….

CZ – The Silver Bullet

That nudge came with CZ, the CEO of Binance. On the 6th of November 2022, CZ announced that Binance would begin liquidating their FTT bags over the course of a few months. This was the beginning of the end for Sam’s empire. CZ had essentially called bullshit on Alameda, and his announcement set in motion a series of events that caused one of the biggest meltdowns the crypto market has ever seen.

16 minutes after CZ’s tweet, Caroline Ellison, CEO of Alameda, tweeted this:

Cryptonary’s initial reaction when we saw this tweet was, “with what funds?”.

Why specifically $22 when Caroline clearly knew the CZ announcement would cause a dump? Why not pick them up cheaper if they wanted them?

We knew Alameda was predatory - who were they trying to protect here?

It certainly wasn’t the market.

It was clear at this point that the fears were true – Alameda’s financial health was tied to the market cap of FTT, and Caroline’s offer was a last-ditch attempt to avert disaster.

In other words, the gig was up.

The collapse of Alameda would have been relatively damaging for markets on its own but likely manageable. Unlike 3AC or Terra, Alameda did not have large BTC and ETH holdings that could be dumped on the market. Alameda Research could have disappeared into nothing, and other than some damage to altcoin projects and market liquidity, in general, things would have been ok.

But this was not the case. As it turns out, Alameda failed months ago – possibly as early as May 2022.

Complete Degeneracy

The truth was (we’ll be hearing a lot more about this over the course of the coming months) FTX had been sponging Alameda’s HUGE losses for months. How?Alameda had been accumulating a huge margin position through FTX – well beyond what any other borrower could possibly have accrued without being liquidated. Alameda had been using these funds to cover losses (potentially accrued through the collapse of LUNA earlier this year), bad venture capital investments, and probable huge losses running unprofitable market-making operations in a bear market (covering liquidations, etc.).

However, the “special relationship” between FTX and Alameda went well beyond what anyone could have imagined.

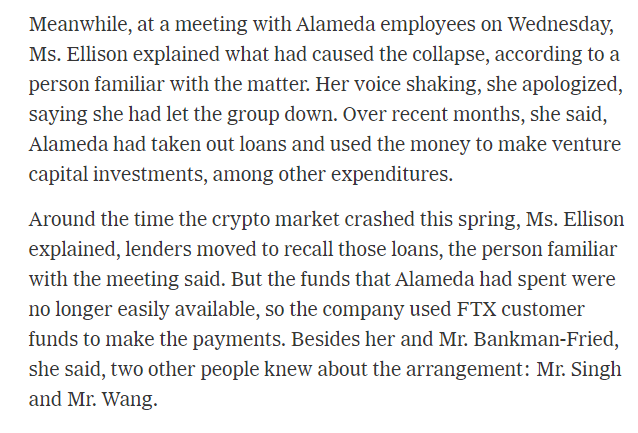

Around springtime 2022 (confirmed by Caroline in an internal meeting), external lenders had attempted to recall their loans to Alameda, which didn’t have the funds - or they were no longer liquid (vested, etc.). At some point, Alameda was unable to fund itself, and so FTX most likely started using their own reserves to backstop Alameda's losses and pay down these loans.

Alameda was clearly burning cash at a rate neither they or FTX’s revenue stream could keep up with, so somewhere along the line Sam OK’d the use of FTX customer funds to pay down these loans in an absolutely disgusting, fraudulent, and criminal act that has left quite literally millions of FTX customers cumulatively short billions of dollars in assets.

This essentially turned FTX/Alameda into a Ponzi scheme where external funds were required to keep the operation flowing. If FTX had to resort to using customer funds, their revenue was clearly not enough, and existing customer deposits could only last so long. Now, this is a fair amount of speculation on our part, but we believe that it had to have panned out along these lines. There’s no other obvious reason for FTX to begin using customer funds. However, FTX couldn’t just directly give Alameda assets – there had to be some sort of collateral used…

Remember the FTT token situation we outlined above? Clearly, Sam knew that Alameda was struggling and so began transferring locked FTT to Alameda in large quantities – likely from his own holdings. He knew these tokens would be unlocked in September. This was an attempt to fill the large gap in Alameda’s balance sheet. Those FTT buy and burn tweets start to look extremely malicious – an attempt to get retail to purchase FTT to help prop up its price since both Alameda and FTX were now dependent on it not crashing.

Why was FTX dependent on FTT not crashing? Here's the most gruesome part – no other lender was likely to take FTT as collateral for loans. We can name one though…. FTX itself! FTX takes their imaginary printed tokens as collateral for “loans” to Alameda, funded by customer deposits. The degeneracy, fraud, and criminality here are astounding. Obviously, this is all after the fact, and we still don’t know the finer details. Whatever the case, the situation was a ticking timebomb.

FTX Collapse – as it happened

We’ve established that Sam’s empire was doomed the moment CZ tweeted he was liquidating FTT holdings. However, the collapse of FTX exchange was still questionable to the outside world at this point. After the CZ tweet, users began withdrawing from FTX en masse in one of the biggest bank runs a crypto exchange has ever seen – in 24 hours the number of BTC in the exchange’s wallets dropped from just under 20,000 to a mere 36. Over $5 billion in total assets were withdrawn just on Sunday the 8th of November.Even at this point though, Sam continued to play the card that FTX was perfectly solvent and had indeed been fulfilling the large withdrawal requests for at least a day:

On Monday the 7th of November, SBF (perjuring himself in what appears to be a last-ditch effort to slow the tide of withdrawals) tweeted that FTX had enough to cover all client holdings and hadn’t been investing them (even in treasuries, because that would have been too risky…). Meanwhile, the official FTX account was Tweeting BS like this:

More lies, more deceit, right up to the very end.

Customer withdrawals were still marked as processing right up until Tuesday the 8th when FTX officially suspended withdrawals – as confirmed by an FTX support employee... via Telegram. It should be noted that this announcement didn’t come from SBF, the official FTX account, or any of the other official channels (even email). Complete radio silence.

Even worse, deposits remained open, and so some users continued to deposit even though there was no hope of them getting their funds back off the exchange. Unless you were active on Crypto Twitter or Telegram, there was no way of knowing what was unfolding – sick.

In a shock tweet, CZ stated that FTX had asked them for help on the afternoon of Tuesday 8th November:

The idea was that Binance would acquire FTX.com (FTX.us remained unaffected due to US regulation) in full and backstop any customer liquidity shortages. This breathed an air of hope into the market and, more specifically, FTX customers who were now stuck. However, the deal was subject to corporate due diligence checks. And so, the market could do nothing but wait.

A day later (9th November), the pain came:

Now it’s important to note that Binance/CZ was likely under a non-disclosure agreement to gain permission to scrutinize FTX’s books. So, we believe the thread above was an attempt to provide as much information as possible without going into specifics. TLDR:

- Note the “latest news reports… alleged US agency investigations…” statement – translated to “we know they’ve been mishandling customer funds; it’s a shitshow”.

- “…the issues are beyond our control or ability to help” – translated to “fucked beyond repair”.

On Friday the 11th of November, SBF tweeted that he had filed for Chapter 11 bankruptcy for FTX.com, FTX.us, Alameda Research, and various other subsidiaries:

That process is underway and basically will be a long and drawn-out situation that will likely take years. One probability, similar to the Mt.Gox proceedings, is that anyone who used FTX.com/us will likely be publicly doxed.

But just how bad were FTX’s finances?

Aftermath

Reports are that the FTX balance sheet was an absolute disaster. Allegedly, the day before the bankruptcy, FTX had a mere $900 million in liquid assets against $9 billion in liabilities – a massive $8 billion hole in its finances, and much worse than the initially speculated $6 billion. There are several reports that FTX loaned as much as $10 billion of customer funds to Alameda – an incomprehensible number, and a decision that SBF has said was a “poor judgement call” (disgusting). There has been a recurring theme in SBF’s tweets where he shoots for sympathy:Cryptonary simply doesn’t accept this. The actions on the part of senior management of both FTX and Alameda were pre-meditated, malicious from the start, and were fully intended to abuse a position of power and trust that customers and investors had placed them in. They abused their standing within the community and beyond - both for their own gain and then to cover up their numerous mistakes. Jail, no other acceptable outcome.

To add further fuel to the fire, after the bankruptcy, FTX was allegedly hacked, and up to $600 million of the remaining funds on the exchange were drained out of exchange wallets in “unauthorised transactions”:

Whether or not this was an inside job is unknown at this point, and we’ll refrain from speculation. However, we found a thread that followed updates as it happened that may be interesting to readers:

In the days after SBF’s Twitter account took a strange turn where he began tweeting single letters, spelling out “what happened” over the course of 24 hours:

This appears to have been a narcissistic attempt at fooling a tweet-scanning bot – it’s been confirmed SBF was deleting an incriminating tweet at the same time as every one of the above tweets.

We’ll re-iterate – over one million individuals have likely been affected by the FTX insolvency. It’s all fine and well for Sam to be sitting in his $30 million mansion in the Bahamas playing League of Legends, but to actively taunt (for lack of a better word) those users and customers, as well as investors, in a poor attempt to cover his own tracks on a platform that many are eagerly waiting for useful information from him is sociopathic.

These developments were just the immediate aftermath of the collapse of FTX – there are other, likely longer-lasting effects that are still to play out. We’ll be keeping an eye on the situation and posting updates as and when necessary.

Contagion

The number one issue with an event of this scale is the contagion effect that follows. We witnessed it with the LUNA collapse earlier this year, and we will no doubt see a similar cascade in the weeks and months to come. One of the first crypto-based firms to announce FTX-related issues was BlockFi, a centralised crypto wealth management firm involved with SBF:

BlockFi had previously agreed a $400 million line of credit with SBF earlier this year, and with his empire in bankruptcy, that line of credit no longer exists. BlockFi was preparing for bankruptcy as of the 15th of November. It’s unclear what happens to that platform and its customers going forward.

What is clear, however, is that the web of financial partnerships and investments that Alameda and FTX has built up over the last few years will be brought to attention, and there will be casualties – both within DeFi, and crypto CeFi.

Project Insolvencies & Bank Runs

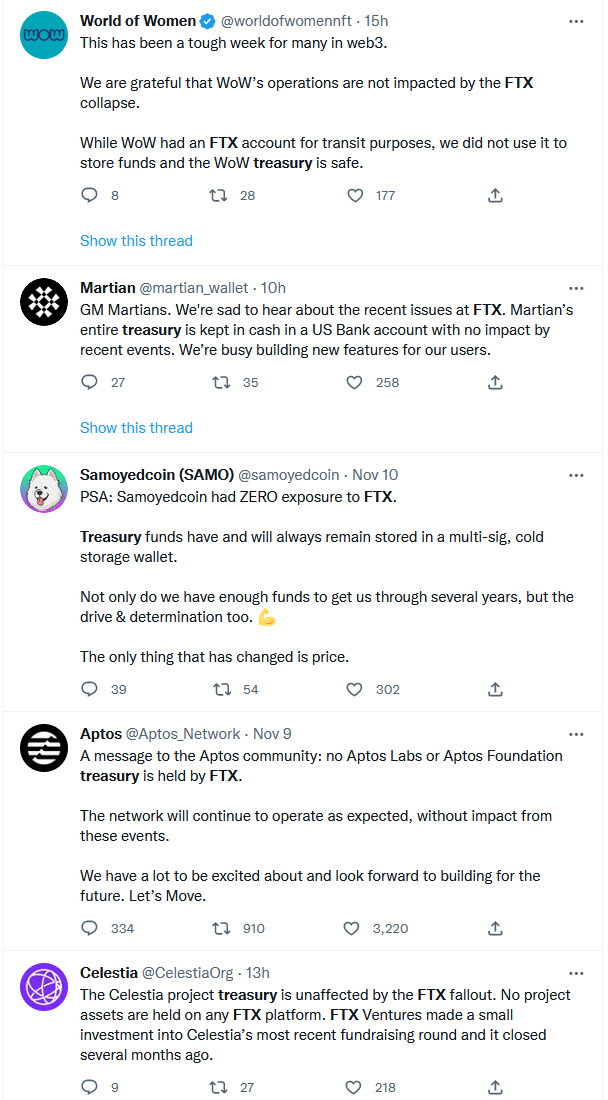

Many DeFi projects, and crypto funds, had their treasuries on FTX. One key actionable point is to check if any of the assets in your portfolio were affected – lots of projects have been making announcements to the contrary but it’s always beneficial to check on-chain, if possible (usually through the project documents):

One of the more important developments over the last few days has been the run on other centralised exchanges. Trust in centralised exchanges is at an all-time low, for obvious, and very valid reasons. The importance of self-custody has become clear for many – last week was Ledger’s biggest week for sales ever. As cliché as it is – NOT your keys, NOT your coins.

Our biggest piece of advice is to take control of your assets – be responsible for your assets and remove the chance for someone else to be irresponsible with them.

Regulation – will the hammer fall?

In recent years, regulators around the world have had a keen eye on the crypto market and, more specifically, DeFi. We believe they have been barking up the wrong tree. It was not a DeFi project that caused this; it was a centralised exchange led by a bunch of charismatic degenerates full to the brim with bullshit that managed to worm their way into the arms of Congress and preach their own agenda. We now know this agenda was malicious. Here’s a video of Sam presenting in front of legislators, explaining exactly what his exchange had been up to almost word for word (the audacity):

We knew that it was likely legislators would use this as a battle cry for stricter regulation on crypto in general, with US Treasury secretary Yellen saying that the FTX collapse strengthened her view that the crypto market needs tighter regulation. However, we would argue that it was strict regulation that amplified the damage done to US/UK/EU consumers.

The decision to ban derivatives largely pushed otherwise protected consumers away from FTX.us and on to the international product, FTX.com. Another key factor was that many of the tokens that US citizens wanted to trade were banned in the US, and so the only option for many to acquire these tokens was to go to the international products via VPN or other methods.

This begs the question – if users can navigate VPNs to get on the international product, this is a lot of extra, risky, unnecessary steps. Why not just use DeFi? Now, it could be argued that there is not enough liquidity on DEXs to fulfil large orders without high slippage etc. Yes, for the most part, the UI/UX on DEXs still has a ways to go before they can be truly competitive with the CEX experience. But how much unknown risk are users taking on by holding their assets in these centralised, supposedly trustworthy companies?

As we have seen repeatedly, regulation of centralised actors within the crypto space is required because the crypto market is not mature enough to self-regulate. DeFi’s main problem (other than obvious rugs) is developer incompetence (e.g. Nomad) and flawed logic (e.g. LUNA/UST). Audits are becoming more mainstream within the space, especially within the last year

Having said that, without regulations, many more US consumers would have fallen victim to the FTX liquidation – FTX.us was not immediately affected by the collapse of FTX International since US regulations dictate that exchanges must have customer deposits backed 1:1 at all times. FTX.us users were withdrawing right up to the bankruptcy on the 11th of November.

Gary Gensler would love nothing more than to brand all crypto assets other than BTC as securities – but does he have that mandate? The collapse of a centralised Ponzi scheme means that they should be asking questions about CeFi actors more than DeFi actors.

Very few (notable) DeFi projects have been fumbling customer funds intentionally (other than exploits) because everyone can see exactly where those funds are always – the same should be true for CEXs and other centralised platforms. NO CENTRALISED CRYPTO CUSTODIAL ENTITY SHOULD EVER BE INSOLVENT. They make enough money from fees; it is pure greed to utilise customer funds for anything they haven’t agreed to beforehand for their own profit, or that of investors.

Also, regulation only works for those concerned about breaking the law. Not sure this was ever the case for SBF & co.

Conclusions

One of the biggest takeaways from this event is that we are all susceptible to BS in one form or another. Between us, the team at Cryptonary easily has 50+ years of combined experience in this market. Yet, many of us were caught off guard and subsequently lost funds. As soon as we believed there could be issues, Cryptonary warned members to remove any assets from FTX ASAP. However, some assets couldn’t be moved in time – for example, staked assets with a time lock, etc.Another key point is never to take anything at face value – this goes for the good and the bad. When CZ tweeted that Binance was to begin dumping FTT and refused to take Caroline’s offer of buying the whole batch, there was backlash on Crypto Twitter. Why would CZ do this? Clearly a predatory attack on a competitor’s exchange token. But was it?

He saw through the BS, caught SBF in 4K, and had the means to act on it.

It is very likely that CZ prevented a potentially apocalyptic version of last week’s events further down the line. We believe that SBF was close to getting away with it. Think about it:

- We know that SBF was lobbying with regulators on prohibitive laws that would have worked in FTX’s favour, essentially banning competition.

- We know that FTX was working on a stablecoin – backed by the same garbage and shenanigans outlined above? A method to plug the $8b hole he had created?

But Cryptonary, were you not shilling FTX?

We see a lot of you talk about "Cryptonary you pushed FTX as a great exchange" so here's us addressing it outside of DMs and comments.Yes, we did push FTX similar to how we'd push towards any product we use (Ledger, Argent...). Why? Because FTX truly was a great exchange and we started using it in 2020/2021 because they were superior in our opinion.

An FTX insolvency was very unlikely in almost everyone's head. Especially as SBF was generally a good actor in crypto. He saved Sushiswap, helped Solana, saved the market from the Voyager unwind and helped BlockFi. Someone who does that is unlikely to illegally use people's funds but obviously he did.

It's like saying Jeff Bezos is taking people's items and selling them on the black market in secret. Definitely possible but extremely unlikely coming from him.

When news came out about the insolvency, and it was still just rumoured, we did say that it's definitely not worth finding out with your funds. Our research team spotted the threat early on, releasing an urgent notice to all members via Discord and email that they should withdraw their funds from FTX.

We are grateful that most of our community managed to get out prior to the pausing of withdrawals. For those that didn’t, we understand how difficult this time is, and whilst the mission has never been clearer, that isn’t all that comforting when you’re down bad.

Recommended from Cryptonary