Save 23% ($351) & Get a Free 1-1 Call with our Team ⏰ : 0d 2h 59m 44s

Guide: Impermanent Loss

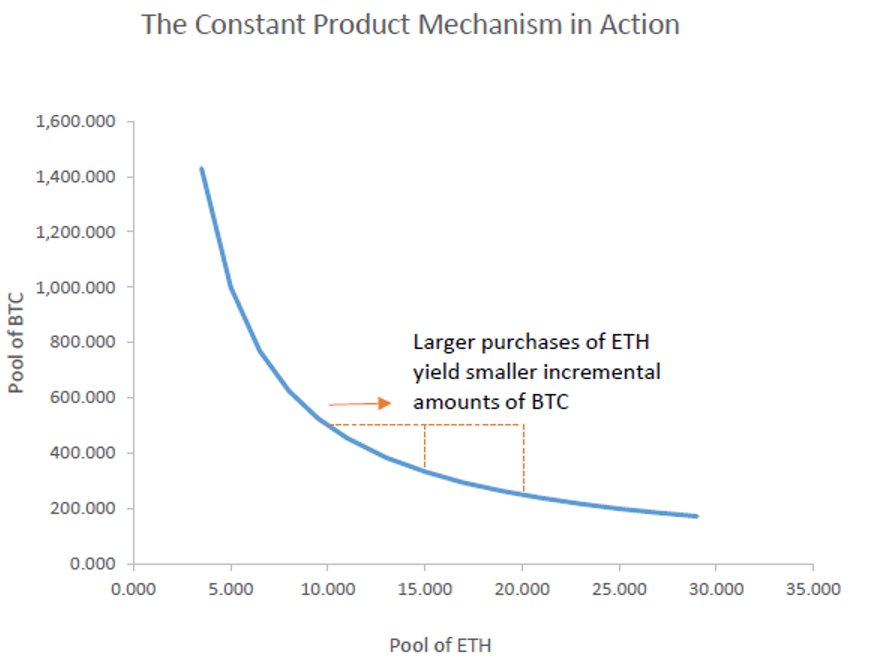

The above diagram shows an example of what happens to a BTC/ETH liquidity pool as ETH is added to the pool in return for BTC. Notice that the more ETH is added to the pool, the less BTC there is, and therefore the less BTC that is gained by adding more ETH. If a pool becomes unbalanced, then arbitrage traders see an opportunity to add more BTC to the pool, which would yield substantially more ETH in proportion to the USD value. Thus, it is arbitrage that keeps the pools balanced, rather than any internal mechanism.

What is Impermanent Loss?

Most, if not all, Automated Market Makers (AMMs) such as Uniswap, THORChain, and Serum DEX, use liquidity pools to determine the price of assets. The idea of a liquidity pool is that anyone can come along and deposit one asset and take another asset of equal value out. This is why it is called a swap: the user is literally swapping one asset for another rather than placing bids or askings on an order book.

As with most yield bearing investments, your capital is at risk through natural price action. However, when providing liquidity to an LP, this can also lead to something called ‘Impermanent Loss’.

Impermanent Loss is a phenomenon unique to liquidity pools whereby liquidity providers can sometimes end up with less value than what could have been realised by simply HODLing the staked assets. Here’s a simplified example for a BTC/ETH pool:

- A liquidity pool has 10 BTC and 40 ETH. This implies a Bitcoin price of 4 ETH.

- For this example, we’ll assume Steven enters this pool as a li

It is important to understand this mechanism before making any decisions about allocating capital to a pool. Liquidity providers should consider the length of time they would be holding their stake, the volatility of both assets, and how closely they correlate with each other in order to minimise the chance of realising Impermanent Loss.

Want to learn more about liquidity pools? click here

Disclaimer: THIS IS NOT FINANCIAL OR INVESTMENT ADVICE. Only you are responsible for any capital-related decisions you make and only you are accountable for the results.

Continue reading by joining Cryptonary Pro

$1,548 $1,197/year

Get everything you need to actively manage your portfolio and stay ahead. Ideal for investors seeking regular guidance and access to tools that help make informed decisions.

For your security, all orders are processed on a secured server.

As a Cryptonary Pro subscriber, you also get:

3X Value Guarantee - If cumulative documented upside does not reach 300% during your 12-month membership, you can request a full refund. Terms

24/7 access to experts with 50+ years’ experience

All of our top token picks for 2025

On hand technical analysis on any token of your choice

Weekly livestreams & ask us anything with the team

Daily insights on Macro, Mechanics, and On-chain

Curated list of top upcoming airdrops (free money)

3X Value Guarantee

If cumulative documented upside does not reach 300% during your 12-month membership, you can request a full refund.

Our track record speaks for itself

With over 2.4M tokens and widespread misinformation in crypto, we cut through the noise and consistently find winning assets.

Our track record speaks for itself

With over 2.4M tokens and widespread misinformation in crypto, we cut

through the noise and consistently find winning assets.

Frequently Asked Questions

Can I trust Cryptonary's calls?

Yes. We've consistently identified winners across multiple cycles. Bitcoin under $1,000, Ethereum under $70, Solana under $10, WIF from $0.003 to $5, PopCat from $0.004 to $2, SPX blasting past $1.70, and our latest pick has already 200X'd since June 2025. Everything is timestamped and public record.

Do I need to be an experienced trader or investor to benefit?

No. When we founded Cryptonary in 2017 the market was new to everyone. We intentionally created content that was easy to understand and actionable. That foundational principle is the crux of Cryptonary. Taking complex ideas and opportunities and presenting them in a way a 10 year old could understand.

What makes Cryptonary different from free crypto content on YouTube or Twitter?

Signal vs noise. We filter out 99.9% of garbage projects, provide data backed analysis, and have a proven track record of finding winners. Not to mention since Cryptonary's inception in 2017 we have never taken investment, sponsorship or partnership. Compare this to pretty much everyone else, no track record, and a long list of partnerships that cloud judgements.

Why is there no trial or refund policy?

We share highly sensitive, time-critical research. Once it's out, it can't be "returned." That's why membership is annual only. Crypto success takes time and commitment. If someone is not willing to invest 12 months into their future, there is no place for them at Cryptonary.

Do I get direct access to the Cryptonary team?

Yes. You will have 24/7 to the team that bought you BTC at $1,000, ETH at $70, and SOL at $10. Through our community chats, live Q&As, and member only channels, you can ask questions and interact directly with the team. Our team has over 50 years of combined experience which you can tap into every single day.

How often is content updated?

Daily. We provide real-time updates, weekly reports, emergency alerts, and live Q&As when the markets move fast. In crypto, the market moves fast, in Cryptonary, we move faster.

How does the 3X Value Guarantee work?

We stand behind the value of our research. If the documented upside from our published research during your 12-month membership does not exceed three times (3X) the annual subscription cost, you can request a full refund. Historical context: In every completed market cycle since 2017, cumulative documented upside has exceeded 10X this threshold.

TermsRecommended from Cryptonary